© 2025 Always Buying Scrap! • All Rights Reserved • Website by Chariot

This site protected by reCAPTCHA and the Google Privacy Policy and Term of Service apply.

11 January 2024

In 2023, copper started strong, hitting a $4.35/lb. high. in January. This was followed by a general

downtrend through the rest of the year, with copper hitting a low of $3.50/lb. in October. Copper

finished out 2023 strong, and we are now seeing some positive momentum in the red metal into 2024.

Despite some improvement in industrial output and retail sales, the demand for copper has been

impacted by the weakening Chinese property market. China’s real estate industry accounts for almost

one-third of the country’s copper consumption, which is mainly used in constructing homes. The latest

economic indicators from China, the world’s second-largest economy and top consumer of copper and

other non-ferrous scrap, suggest that deflationary pressures are present. Consumer prices in China

experienced the most significant drop in three years in November, down -.05% y/y vs. -0.2% in Oct. and

down -0.5% m/m vs -0.1% in Oct. China’s worst CPI print in three years raised concerns about the effects

of weak domestic demand on the country’s economic recovery. It is worth noting that China contributes 18% of global GDP.

There has been a decline in the supply of copper due to mining project delays and lower production in

Chile in 2023. Chile is recognized as the leading producer of copper worldwide, with major companies

such as Codelco, BHP, Anglo-American, Glencore, and Antofagasta operating there. Codelco has been

facing operational challenges and high levels of debt, resulting in delays in critical projects that would

have extended the lifespan of their mines. Production at Codelco in 2023 is expected to reach 1.315

million metric tons, which is at the lower end of the estimated range. The company has predicted that

production will begin to recover in 2024 after last year’s output reached a 25-year low.

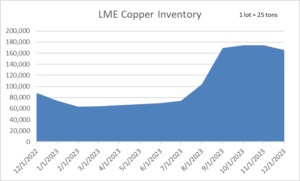

The amount of copper stored at exchange warehouses worldwide has steadily increased since mid-July

2023. As of October 31st, 2023, copper inventories had reached 175k tons, marking a 61.5% increase

since September. This increase follows a 50% rise in August and is believed to be a result of the global

manufacturing slowdown and recession fears affecting commodity prices.

In September, the manufacturing sector in Asia experienced a downturn, and US factory activity

contracted. However, the US job market remained robust, with an unexpected increase in job openings.

The rise in interest rates put pressure on traders and capital-intensive manufacturing businesses, leading

to a trend of minimizing financing costs by depleting stockpiles or selling off metal supplies in the spot

market. As a result, the copper futures curve shifted to a state of contango. Futures contracts trade at a

premium when market participants expect prices for future contracts to be higher than the current spot

price.

Q3 erased gains made by copper early in the year. Declining copper prices were partially attributable to

the appreciation of the US dollar, which reached its highest point of $107.348 in October. A strong dollar

made copper priced in the greenback more expensive for foreign currency holders, particularly in China.

U.S. copper mine production decreased in the first half of 2023 compared to the same period in 2022.

This was mostly attributed to three companies – Freeport-McMoRan Inc., KGHM Polksa Miedź S.A.

Group, and Rio Tinto Group. Production decline was influenced by unplanned maintenance, lower ore

grades, mining rates, record snowfall, and equipment failures. By July 2023, US mine production for the

year had reached an estimated 640,000 tons, indicating a 12% decline from the previous year.

Geopolitical factors have heavily influenced the global copper supply shortage. Peru, the world’s second largest producer of copper, has been dealing with political unrest, including daily rioting, since late 2022.

This turmoil has led to disruptions in supply chains. As a result of protests and roadblocks, major mines,

such as the Chinese owned MMG Las Bamba and Glencore’s Antapaccay, which collectively contribute to

2.5% of the global copper output, have had to limit their production or shut down until March of 2023.

Panama’s recent actions to potentially revoke a contract for one of the world’s biggest copper mines

through a referendum and proposed law have caused concern among investors and resulted in a 40%

drop in First Quantum Minerals’ market value. While lawmakers have attempted to terminate the

contract, the final decision rests with Panama’s top court. This has raised concerns about the future of

copper supplies, as this $10 billion copper mine accounts for 1% of global output and plays a significant

role in the production of electric vehicles.

Towards the end of October, a strike by truck drivers in the Democratic Republic of Congo resulted in the

blockage of nearly 2,700 trucks carrying around 89,000 tons of copper in Kolwezi. This disruption in

supply may cause a shortage of global copper widely used in the construction and power generation

industries. According to a Reuters survey, a minor market surplus this year could become a deficit if the

strike continues. The DRC is the world’s third-biggest copper producer, contributing 10.4% of the global

mined supply last year. The trucker strike has impacted major suppliers like Ivanhoe Mines, CMOC,

Glencore, and Sicomine.

A decline in copper ore grades has made it necessary for miners to extract more ore to obtain the same

amount of copper. Governments have implemented environmental regulations that are causing copper

mining to become more complex and costly by requiring miners to reduce their water usage and

emissions.

With new mines taking years to open due to opposition and delays, some are targeting closed

brownfield mine sites to produce copper faster. Opening brownfield mines remains costly but avoids

destroying new lands, though environmental cleanup is still needed. Reopening a closed brownfield

mine requires over $2 billion in investment. However, the time it saves is substantial. It takes an average

of 15.7 years after discovery for a new mine to begin production commercially. Actual times range from 6

to 32 years, according to S&P Global Intelligence. Compared to developing new mines, building smelters

in China takes only 2-3 years. As a result, there is a supply “paradox.”

Firms predict that 50% of the future copper supply will come from countries like the Democratic

Republic of the Congo, Botswana, and Mongolia, which have higher grades but also obstacles, such as

lack of expertise and their own prevailing laws. Issues in these new supply countries could impact the

copper price index.

With the government spending billions of dollars to replace lead service lines, copper pipelines are

emerging as a safer, more dependable, and sustainable alternative. However, replacing all 12 million

lead and galvanized service lines in America requires over 650 million feet of copper tubing, equivalent

to 180,000 tons of metal. In 2022, the U.S. only produced twenty-two million tons of copper. Upgrading

the nation’s infrastructure will require over $56 billion, far more than the $15 billion currently provided

by the Bipartisan Infrastructure Law.

The growth of renewable energy and electric vehicles has resulted in an enormous demand for copper.

Copper is critical in renewable energy storage systems, solar panels, and wind turbines. It is used in

wiring, busbars, and connectors within solar panels and in generator coils, transformers, and electric

cables of wind turbines. According to The International Energy Agency, wind turbines can require up to 9

tons of copper per M.W., while solar power needs over 3 tons of copper per MW. Similarly, electric

vehicles need over 117 lbs. of copper per M.W., more than the amount of nickel and cobalt combined

and almost six times the amount of lithium required. According to Goldman Sachs, electric vehicles and

charging stations will account for 27% of additional copper consumption over the next decade, rising to

1.5 million tons in 2025.

Copper grades have declined over many years, requiring more ore to produce the same amount of

copper, while environmental regulations are increasing mining costs. Some producers are redeveloping

closed mines to meet growing battery, EV, renewable, and infrastructure demand amid new mine delays.

According to a prominent Chinese copper executive, the global copper market will face a shortage by

2025 as mining lags smelting expansion in Asia. Several reports project a doubling of copper demand by

2035 yet forecast inadequate supply increases, raising concerns of severe shortfalls.

Long-term projections through 2030 for copper pricing and demand remain positive due to the push for

decarbonization and renewable energy by world governments. However, near-term demand depends on

the global economy, particularly China.

In 2024, China will continue to drive global copper demand, while high rates have slowed manufacturing

elsewhere. Operating constraints and smelter maintenance outages in Chile, Indonesia, Sweden, and the

United States capped copper production outside China last year. According to local data provider

Shanghai Metal Market, Shanghai copper inventories remained low for the better part of the year, and

national output rose by 11.5% year-over-year in the first eight months of 2023. March of 2023 saw

monthly refined copper at record levels above 1 million tons. Still, China relies heavily on copper

concentrate imports and needs to import 70% of the input material for copper smelting.

It remains to be determined whether new smelters and capacity expansions in Indonesia, India, and the

United States will compensate for the weakness experienced in those markets throughout 2023. The

ICSG believes that the amount of copper produced from recyclable materials will increase this year

thanks to investment in new secondary smelters and refineries in those countries. Firms like Goldman

Sachs continue to predict that 50% of the copper supply will come from unexpected places like the

Democratic Republic of the Congo, Botswana, and Mongolia. While these countries produce higher

reserve grades, they lack expertise and experience limitations due to their restrictive laws.

A tight balance between copper supply and demand is expected to be seen into 2025 before deficits are

realized as mining lags smelting expansions, capacity, and growth. The ICSG forecasts more than a 4.6%

jump in global refined copper and a 467,000-ton surplus in 2024 as production outpaces usage, but

Western weakness could offset Chinese strength. CRU predicts a deficit of 342,000 tons in 2025, after a

surplus of 260,000 tons expected next year due to rising needs from smelters in China, India, and

Indonesia.

Japan’s Mitsubishi plans a 34% increase in copper output in the second half of the 2023-2024 fiscal year.

The Naoshima Smelter & Refinery in western Japan is expected to increase copper production by about

17% in the second half due to an absence of scheduled maintenance conducted during the previous

year. Copper output at Onahama Smelting & Refining in eastern Japan will rise about 61% into 2024 due

to the completion of a copper joint venture in April of 2023, where it purchased the stakes of DOWA

Holdings and Furukawa Co.

Barrick Gold sees global demand for copper set to surge over the next several years. The company has

stated the desire for copper to account for 30% of its overall profit by the decade’s end. It will accomplish this by expanding its Lumwana Pit mine to double copper production to 240,000 tons annually and through its $7 billion Reko Diq project in Pakistan.

The DXY peaked in October, which made metals priced in U.S. dollars more expensive to holders of other

currencies. The dollar hit a high of 107.34 in October and finished the year at 101.38. A weakened dollar

should begin to ease the expense of copper to foreign buyers.

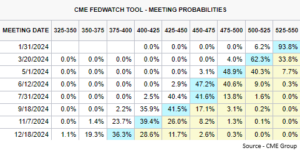

It is expected that the Federal Reserve will lower interest rates in 2024. Before the latest PCE release,

markets were pricing in 6 25bp cuts, equating to a fed-funds rate of 3.75%-4.00%, or a 1.5 percentage

point reduction in the Fed’s target next year. This anticipated policy shift resulted in a stock market and

precious metals rally not seen in many years and an 8% increase in the price of copper in 6 weeks.

Many economists urged some caution as the Federal Reserve would need to see inflation come back

down to target – 2% – to significantly lower interest rates in 2024. The most recent PCE index, the Fed’s

preferred measure of inflation, cooled more than economists had anticipated, bringing the annualized

rates over the past three and six months down to at or below the Fed’s 2% target.

Data showed that the labor market has been cooling in the face of the Fed’s rate hikes from March 2022

to July 2023. However, the U.S. unemployment rate is now at 3.7%, just a 10th of a point above where it

was when the Fed began raising rates. Several factors could halt, or even reverse progress on inflation,

including the extended disruption of traffic through the Suez Canal resulting from Houthi militant attacks

on ships in the Red Sea; a rise in consumer confidence could set up more robust spending ahead. Easier

financial conditions, with the 10-year yield back down to where it was in July when the Fed last raised

rates, could add fuel to borrowing and investment.

Overall, cutting rates stimulates the economy. Provided data over the next few quarters supports a

reduction in interest rates; we should see demand for copper rise as people find homes more affordable

and spend money on home improvements.

Another positive for copper in the coming years is the support of Governments like the USA and China

for solar industries, providing subsidies and other incentives to encourage solar power development.

This has helped to make solar power one of the most cost-competitive forms of energy in China and the

U.S. As a result, solar power is expected to play a significant role in the energy mix in the coming years.

Several Governments support the increasing use of electric vehicles (EVs use significantly more copper

than traditional gasoline-powered vehicles. This growth in EV sales will drive significant demand for

copper.

Environmental regulations are also making copper mining more difficult and expensive, with many

governments requiring miners to reduce their water usage and emissions. Furthermore, social unrest in

mining regions is another challenge that copper miners face, as exemplified by the recent referendum

over Canadian company First Quantum Minerals’ Cobre Panama mine. Making the supply of copper

while increasing the demand for copper should see the value of this red metal appreciate over the next

several years.

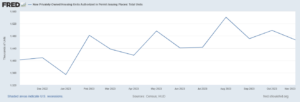

From November 2022 to November 2023, the seasonally adjusted one-year change in privately owned

housing units authorized in permit-issuing places was 4.1%. For privately owned housing units

authorized but not started, the seasonally adjusted one-year change was -8%. Privately owned housing

units saw an increase of 14.8% YOY. Privately-owned housing units under construction at the end of the

period were up .7% for the year when seasonally adjusted. Overall, private housing units completed on a

YOY basis were down -6.2%. The total value of private construction on a YOY basis as of October 2023

(most recent data) was up 9.2%, and total public construction was up 16.4%.

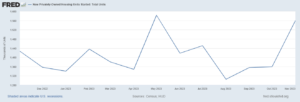

This data tells us that in the private sector, multi-family homes, manufacturing, religious, educational,

and health care accounted for most of the increase. Privately owned housing units saw an increase in

authorization and starts. However, data showed a decrease in the completion of these homes. In the

public sector, power, sewage and waste disposal, conservation and development, and public accounted

for the bulk of the value of construction put in place. On the new home front, more people living under

one building utilize less building space and, therefore, less copper. Manufacturing accounted for 71.6%

of the increase, which is a positive. In the public sector, power accounted for over 50% of the value of

construction put in place in the US, which is also positive.

The trends in public and private housing and construction can be attributable to sticky inflation during

the first half of last year and higher interest rates, which made the costs of purchasing new buildings

prohibitively restrictive. In the back half of 2023, we saw inflation cool, and the expectations of lowered

interest rates eased bond yields. If the Federal Reserve cuts rates next year, we could see some of the

ongoing construction become more affordable to complete, and the demand for buildings go up as

prices come down. This will increase the demand for copper and put positive pressure on pricing.

On Nov 20th, Chinese officials promised support for their country’s property sector, leading to a rise in

copper prices.

Copper has earned the nickname “Dr. Copper” as it has often served as a bellwether for the global

economy’s health. When economies thrive, there is an increased need for copper, while economic

downturns lead to reduced demand. Because of this, the metal has earned the title of a trusted doctor,

prescribing insight into the world’s financial pulse.

On July 31st, 2023, the US Department of Energy (DOE) officially put copper on its critical materials list,

marking the first time a US Government agency has included copper in a “critical” list, following the

examples set by the EU, China, Canada, and many other major economies.

Bank of America’s commodity research team led by Michael Wildmer and Francisco Blanch said copper’s

sensitivity to GDP growth has waned in a recent research note. “As a cyclical asset, copper demand has

always been closely correlated with global GDP growth, but that sensitivity has been declining,” the Bank

of America team said. “This reduced beta to GDP has already provided support to copper prices at

around $8500/t (3.86/lb) in recent quarters and limited downside price pressures on the red metal amid

an industrial recession, a rare occurrence,” they add.

It would prove extremely difficult to predict precisely where copper pricing will end up one year from

now, as many variables and unforeseen geo-political events can occur. This article has outlined some

positive and negative factors that could influence copper pricing over the next one to two years.

Reduced interest rates, decreased inflation, and increased manufacturing and construction are seen as

positives for copper in the near to medium term. Chile, Japan, and China have all increased estimates for

copper production next year. This should be balanced with continued restrictive policies on opening new

mines, production costs for existing mines and smelters, and political unrest that may or may not

continue in top-producing countries.

Making longer-term predictions in copper prices is a more straightforward bet as we know that based on

population growth and projected demand for copper, demand will outpace supply in the medium to long

term. The push to decarbonize the world by top governments through solar and natural energy and

electric vehicles will increase the need for more copper. In addition, the exponential aspect of population

growth means that more housing and buildings will be required. Because of the limited amount of

copper on earth, both in mining and refining capacity, there will not be enough copper to satisfy the

demand, and copper prices should appreciate considerably.

What is Recycling and Composting? Recycling is the process of converting waste...

The Journey of Your Trash: What Happens After You Recycle? Ever wonder what happens to...

The growth of Artificial Intelligence (AI) has accelerated exponentially in recent years due to...

What is Recycling and Composting? Recycling is the process of converting waste...

The Journey of Your Trash: What Happens After You Recycle? Ever wonder what happens to...

The growth of Artificial Intelligence (AI) has accelerated exponentially in recent years due to...

As a family-owned business, we treat you with integrity and respect.

8:00am to 4:30pm

Last customer will be let in the gate at 4:15pm.

8:00am to 12:00pm

Last customer will be let in the gate at 11:30am.

© 2025 Always Buying Scrap! • All Rights Reserved • Website by Chariot

This site protected by reCAPTCHA and the Google Privacy Policy and Term of Service apply.